Blockchain

The blockchain is a digital ledger that stores the transactions happening in the Bitcoin network

The blockchain is a digital ledger that stores the transactions happening in the Bitcoin network. A ledger is basically a book or collection of financial data.

The notepad in your drawer where you record your expenses is a ledger.

The Excel file in your computer where you store your savings is a ledger.

Even the transactions you note down on a napkin can be considered a ledger.

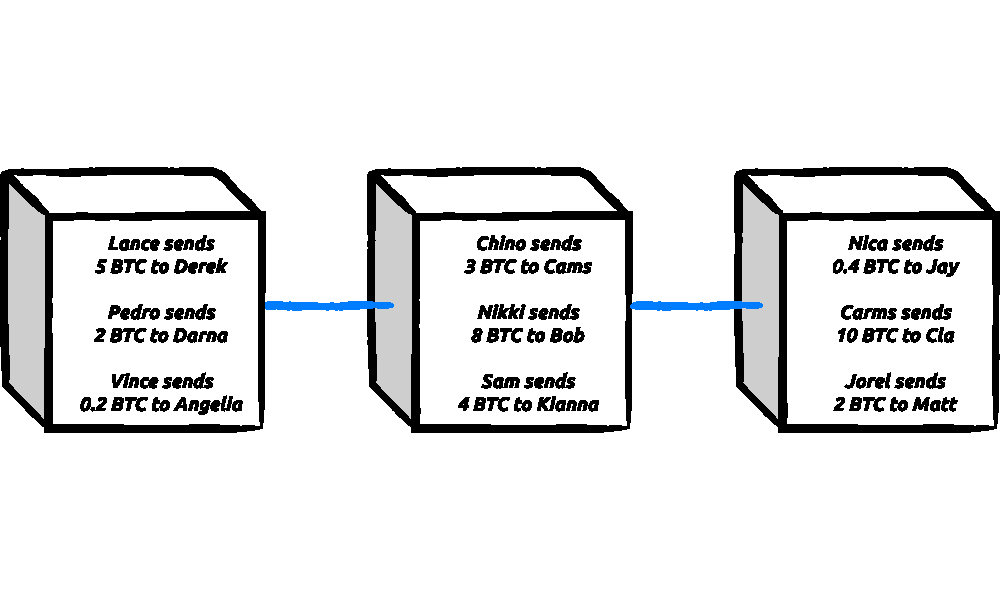

So what makes the blockchain so special? It’s the fact that transactions are stored in the form of blocks and are secured by cryptography.

You can think of the blockchain as a chain that ties all the transactions together one after the other. The blockchain is immutable, decentralized, distributed, secure, and fully verifiable.

How does the blockchain work?

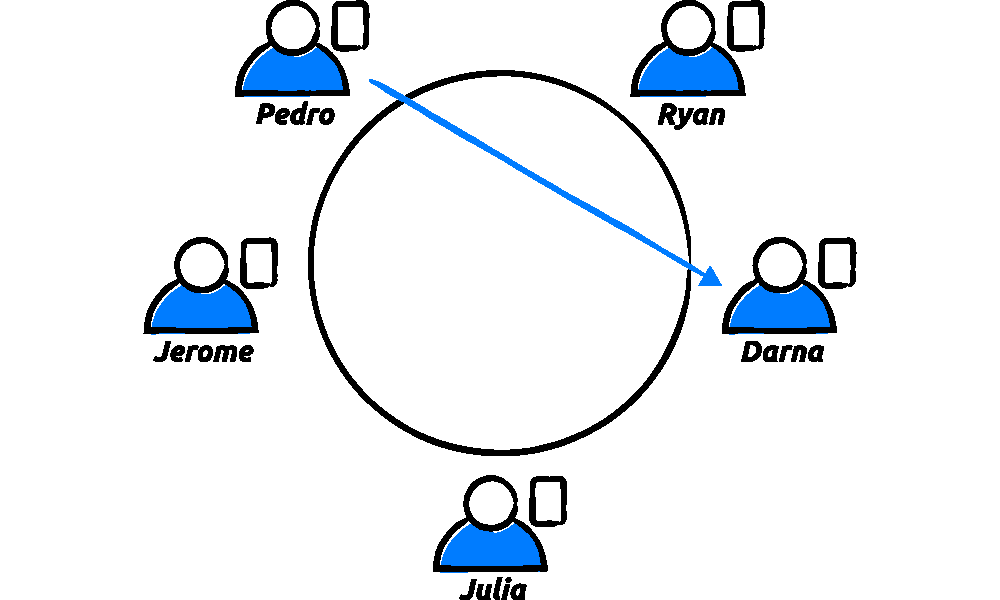

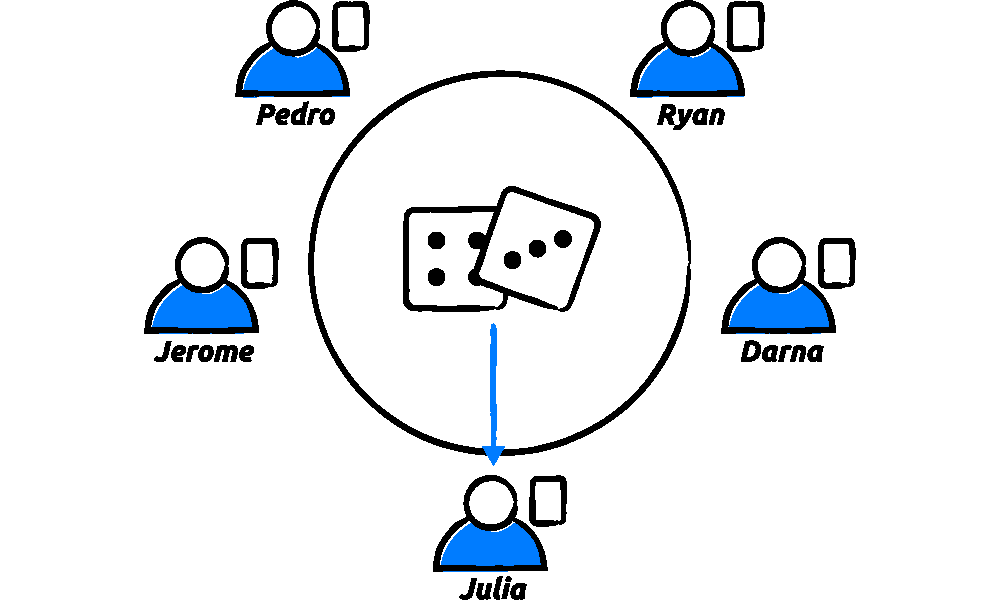

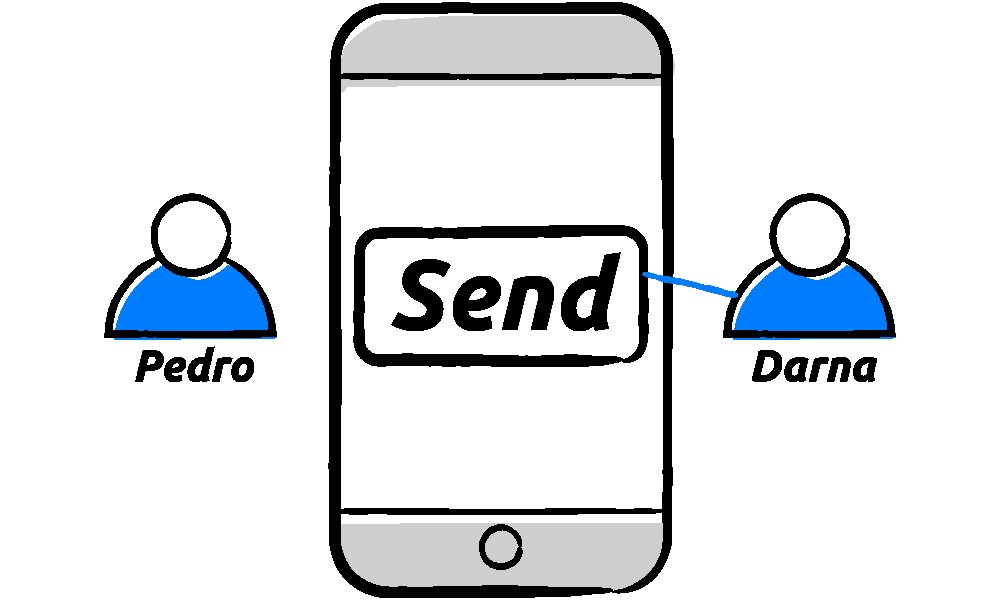

Let’s start with a simple example: Imagine a table of five people who are all with their own notebooks. Let’s name them Pedro, Darna, Julia, Jerome, and Ryan. They’re strangers to one another, which means there’s no trust among them whatsoever.

Pedro wants to send two (2) bitcoin to Darna. For that to happen, all five people must agree that the transaction is valid.

A lottery happens where a random person is chosen to verify the transaction.

For this example, let’s imagine that Julia was selected by the lottery.

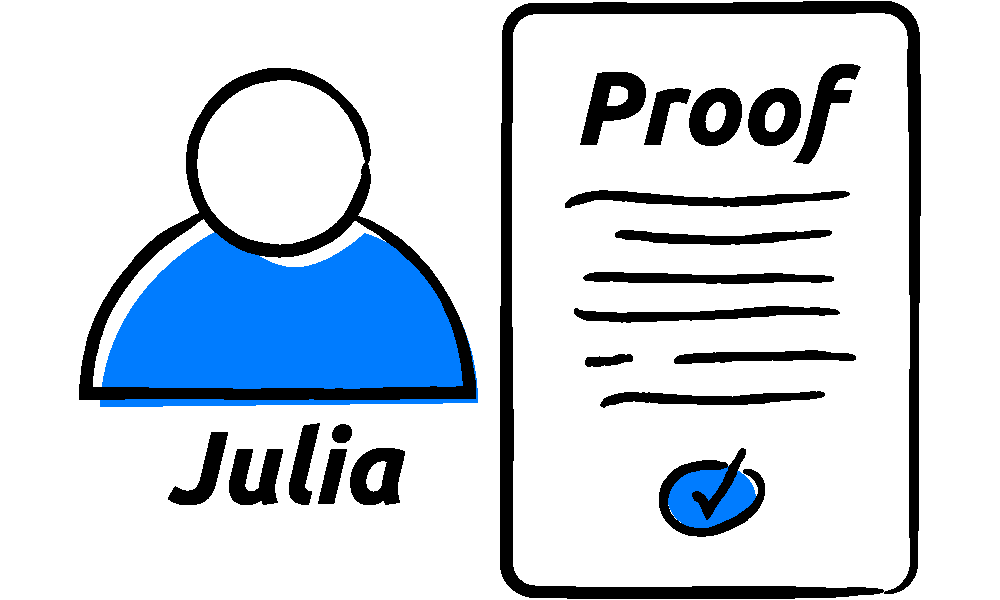

Now, Julia has to verify Pedro’s transaction to see if it’s valid. As soon as she does, Julia must show proof to everyone else at the table that she has completed the verification.

All the other five people must agree with Julia’s proof. If they see that Julia had made a mistake, the lottery will re-roll and choose another person for the job.

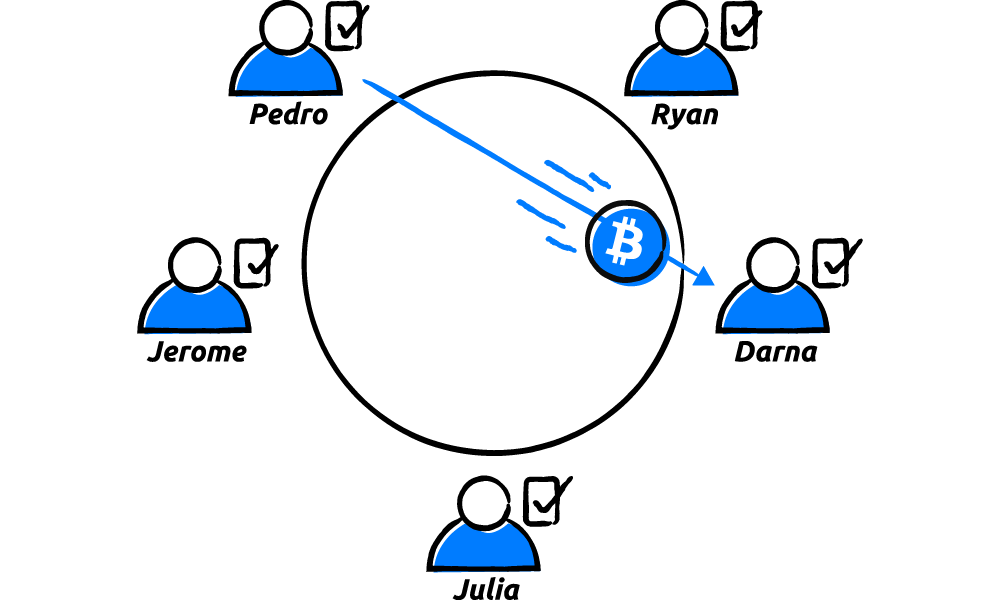

But if they do agree, all five of them must record Pedro’s transaction and Julia’s proof on their notebooks. After that, Pedro’s two (2) bitcoin are sent and the people at the table then move on to the next transaction.

Bitcoin works just like this. Each user has an identical copy of the blockchain, which is the notebook in our example. In this notebook, all transactions in the network are recorded and constantly compared with everyone else to ensure integrity in the network. This process happens repeatedly every day, keeping the Bitcoin network alive and secure.

Transferring monetary value over the Internet in a decentralized fashion was never possible in the history of mankind until Bitcoin came along.

Of course, this is just a simplified version of how Bitcoin’s blockchain works. So let’s take a closer look at how everything really happens, starting with the five people we mentioned.

Bitcoin Mining

The act of validating transactions is referred to as mining. In the example above, Pedro, Julia, Jerome, Darna, and Ryan are what we call miners.

A Bitcoin miner is a computer running the Bitcoin client which helps verify and record the transactions happening in the blockchain. Think of miners as the “auditors” of the network — making sure each transaction is valid before it pushes through.

A miner can refer to both the computers running the Bitcoin client or the people managing them.

Bitcoin mining is totally location agnostic, which means anyone anywhere in the world can participate as a miner — you, your neighbor, even the sari-sari store vendor outside your house right now. Anyone with a computer can be a miner. Bitcoin is open to everyone.

In the actual Bitcoin network, there are thousands of Bitcoin miners spread across the world. As of writing, more of the miners are located in the United States, Russia, Germany, and China.

Blockchain, but a little more technical

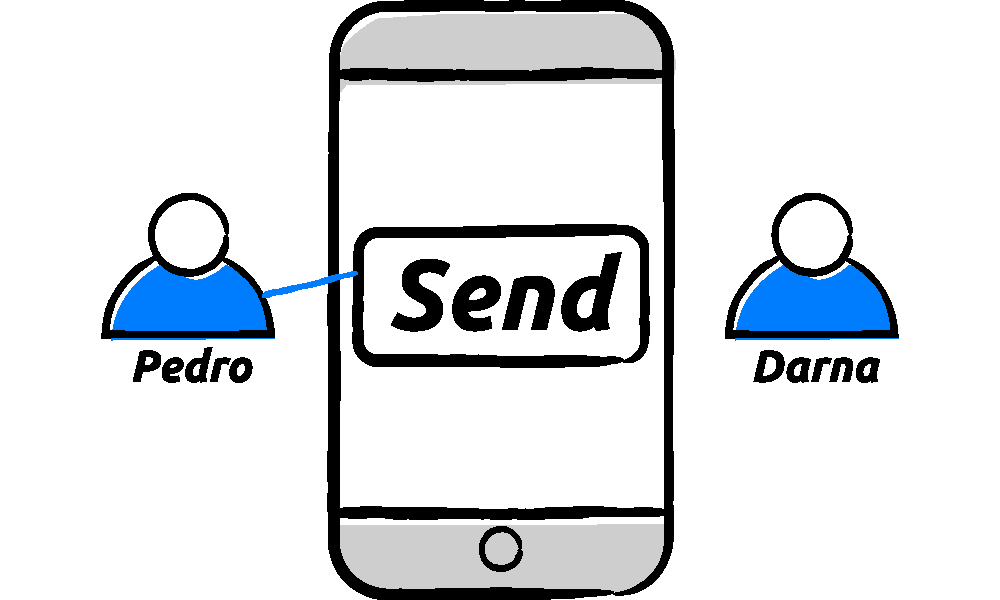

Let’s revisit our previous example and add some more details. Remember Pedro? He wants to send Darna two (2) bitcoin again.

Step 1: Pedro presses “send” using his Bitcoin wallet.

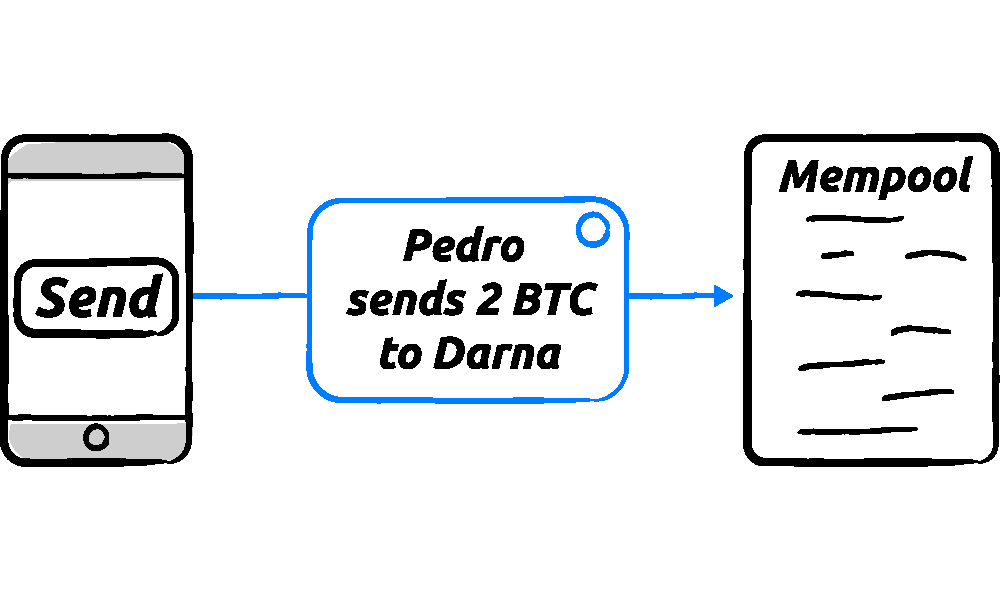

Step 2: Once it has been verified by the network, the transaction information is sent to a pending transaction pool called the mempool.

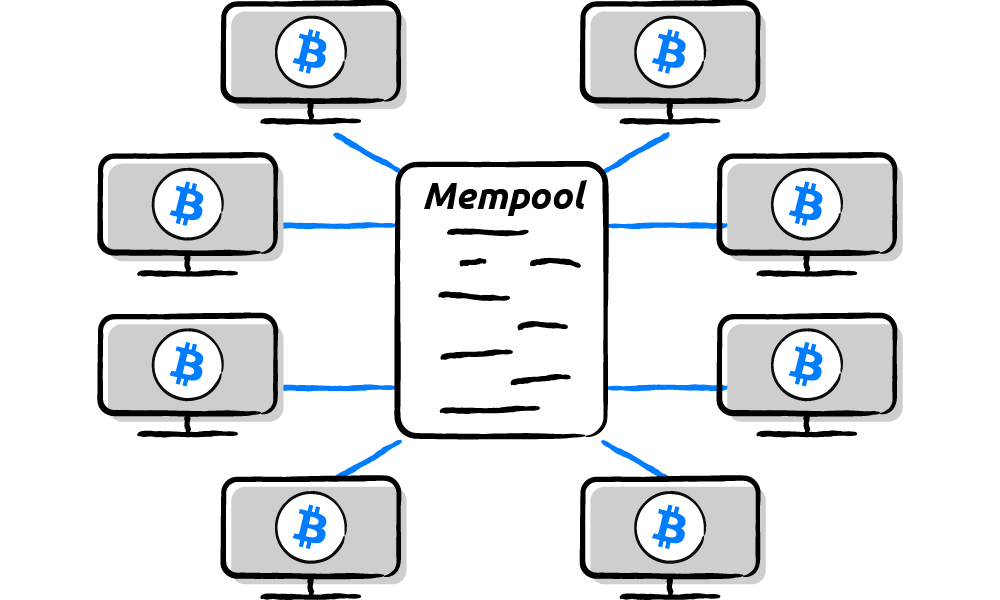

Step 3: Miners around the globe validate these transactions at a certain pace with a process called hashing. The hashing process is random just like a lottery.

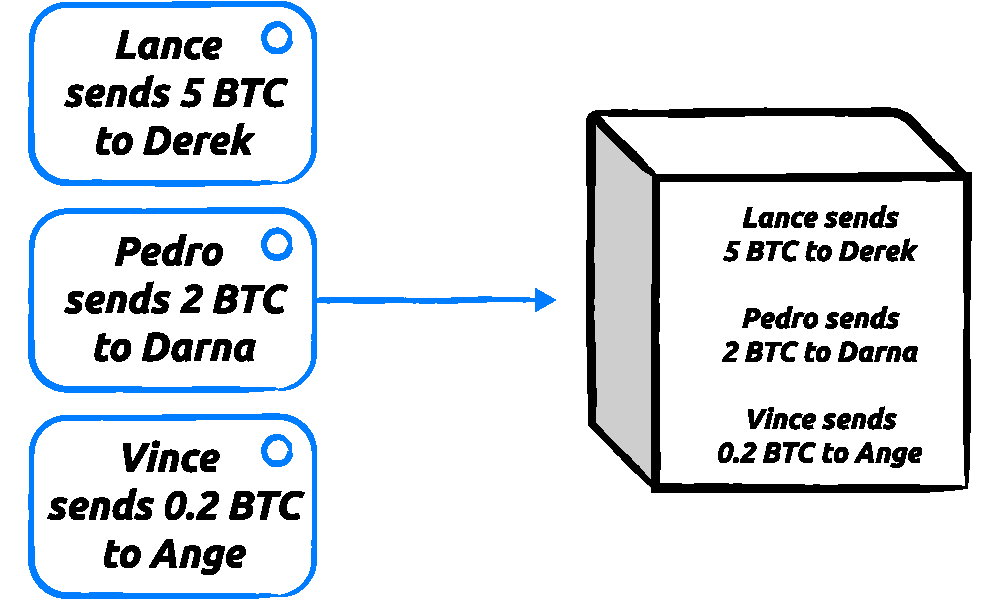

Step 4: Once the miners give Pedro and other people’s transactions the OK signal, they are clustered into a block.

Step 5: After clustering them together, the block is added on top of previous blocks which contain previous transactions, forming a chain. These blocks are all mathematically linked to each other to keep them secure.

Step 6: Darna receives the two (2) bitcoin Pedro sent.

Step 7: The miner who first validated the transaction receives bitcoin as compensation. This is what you call the block reward.

This whole process is based on a Proof-of-Work or PoW consensus mechanism. PoW is a consensus mechanism describing the computational power and electricity miners need to validate transactions.

Here we can see how Pedro and Darna were able to transfer value between each other without the need for third-party interference — no more middlemen, hefty fees, long wait times, or logistical problems.

Aside from these, what are the other benefits of a blockchain?

Benefits of Bitcoin’s blockchain

- Transparent: All transactions happening in the network are publicized. All you have to do is look it up online.

- Immutable: Transactions happening in the network are stored in the form of blocks and are secured by cryptography. This makes the network impossible to manipulate, tamper, or hack.

- Efficient: The blockchain facilitates transactions more efficiently while maintaining decentralization, as opposed to the traditional means of sending money which is prone to human error, legal roadblocks, or intervention.

- Decentralized: The blockchain does not have any central authority or entity. There is no single point of failure.

This whole process happens constantly in the Bitcoin network every single day. As of 2021, Bitcoin is responsible for transacting billions of dollars and connecting all kinds of people worldwide.

Powered by Bitskwela

Don’t have GCash yet?

Got more questions about Crypto and NFTs?

Check out our GCrypto Learning Hub to learn more!